Say hello to flexible credit that suits you with Argos Pay

After one simple application you can use Argos Pay again and again at Argos or Habitat. Apply now or apply during checkout today. You can check your eligibility without impacting your credit score.

Argos Card customer? Your Argos Card has updated automatically to Argos Pay. Register to start using.

Existing customer?

Argos Pay customers - FAQs below or manage your account by logging in now.

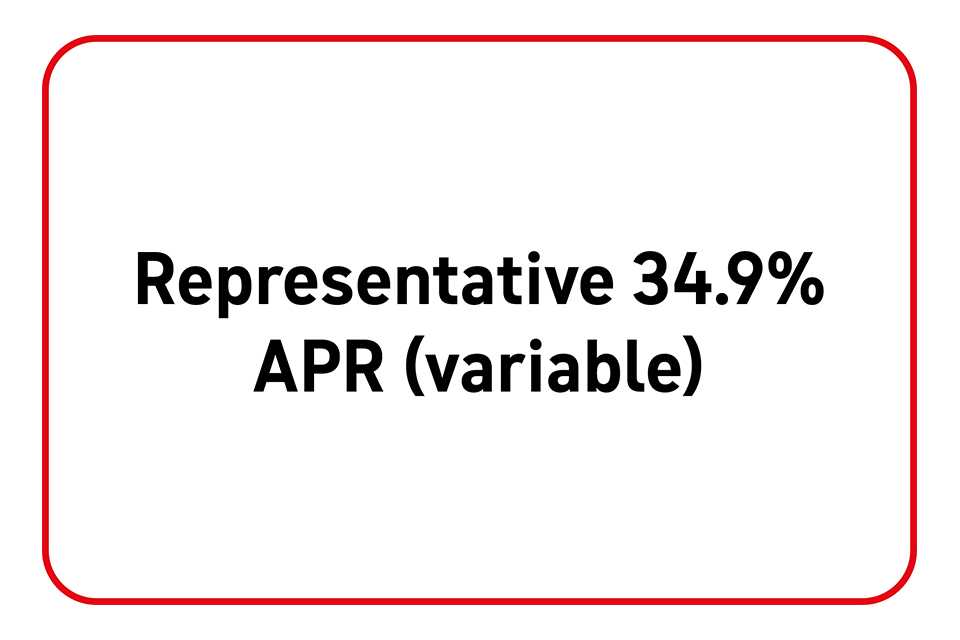

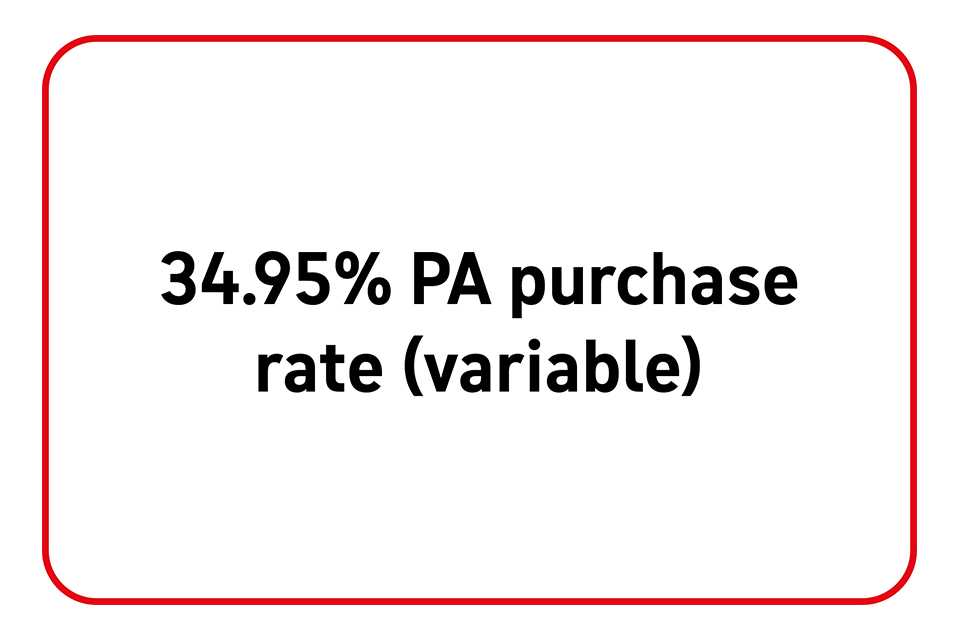

Argos Pay Representative Example

Offers and credit subject to status, 18+, UK only, NewDay Ltd. Your APR and credit limit will depend on the assessment of your application. Terms apply.

Argos Limited acts as a credit broker for NewDay Ltd and is not a lender.

Benefits

Apply once, shop anytime

Use your account again and again without having to reapply each time.

Fair and flexible

All plans are clear and transparent with no early repayment fees.

Stay in control with the app

Set up spending alerts and get a clear view of everything in one place.

Discover options to pay later

Buy Now, Pay Later with 3 to 12 months 0% Interest.

At your own pace. Pay the minimum each month, and more when you can, just like you would on a credit card.

Pick a plan-up to 48 months-and pay the same amount each month. Easy.

0% interest for up to 36 months with fixed monthly payments.

Terms apply. The promotional offers available to you will be based on the item(s) in your trolley and our assessment of your circumstances.

How to apply for Argos Pay

Apply during checkout today

1. Add item(s) to your trolley then choose Argos Pay when you come to pay.

2. Complete an eligibility check so we can show you what plans, credit limit and offers you're eligible for. If you're happy, go ahead and complete your application.

3. See your payment options and pick one. What you're offered will depend on what's in your trolley and the outcome of your application.

Apply now

1. Complete an eligibility check so we can show you what plans, credit limit and offers you're eligible for. If you're happy, go ahead and complete your application.

2. Add item(s) to your trolley then choose Argos Pay when you come to pay.

3. See your payment options and pick one. What you're offered will depend on what's in your trolley and outcome of your application.

To apply, you must:

- Have lived in the UK for at least a year and be 18 years old or over

- Have a UK mobile and email address

- Not already have an Argos Card or Argos Pay account

Argos Pay FAQs

You can find all frequently asked questions here.

Haven't found what you're looking for? You can find more information on our FAQ's.

Alternatively, you can call Argos Pay customer helpline on 0333 240 8002. Opening times are 9am - 7pm Monday to Friday and 9am - 5pm Saturday. Please have your account number ready when you call. You can find your account number within emails and an SMS sent to you by Argos Pay shortly after opening your account.

Calls are charged at the standard national rate. Call costs from mobiles and other operators may vary so please check before calling. Calls may be recorded and monitored for training and security purposes and to help us manage your account.

Argos Pay

Argos Pay is provided by NewDay Ltd. UK residents aged 18 and over. Offers and credit subject to status. Terms apply. Argos Limited is a credit broker and not a lender, introducing Argos Pay under an exclusive arrangement with the lender NewDay Ltd.

Argos Limited does not earn an upfront commission for introducing customers to NewDay Ltd. Argos receives remuneration as part of the wider relationship with NewDay that is not calculated on an individual customer level.

Argos Limited is authorised and regulated by the Financial Conduct Authority (firm reference number: 713206), registered office: 33 Charterhouse Street, London, EC1M 6HA.

NewDay Ltd is a company registered in England and Wales (company number: 7297722), registered office: 7 Handyside Street, London, N1C 4DA. NewDay Ltd is authorised and regulated by the Financial Conduct Authority (firm reference number: 690292) and is also authorised by the Financial Conduct Authority under the Payment Services Regulations 2017 (firm reference number: 555318) for the provision of payment services.